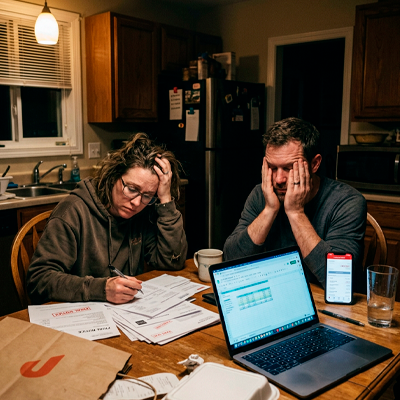

For many Americans, financial pressure no longer comes only from major emergencies or dramatic life events. In a growing number of households, the real damage happens slowly through small decisions that barely feel expensive in the moment.

A food delivery order after work.

A financed smartphone upgrade.

A streaming bundle nobody fully uses.

A grocery trip filled with “quick convenience” purchases.

None of these choices seem financially dangerous alone. But together, they quietly reshape monthly budgets in ways many middle class families underestimate until savings accounts stop growing and credit card balances become harder to control.

What makes this shift especially difficult to notice is that modern spending rarely feels irresponsible. Most purchases now arrive wrapped in convenience, comfort, time-saving promises, or emotional justification.

A family can earn over $90,000 per year and still feel permanently behind financially because recurring lifestyle costs expanded faster than income.

That pattern became increasingly common across the United States over the last few years, especially as inflation pushed everyday essentials higher while subscription-based spending quietly exploded in the background.

Small Financial Habits That Create Surprisingly Expensive Months

One major budgeting mistake comes from focusing only on large expenses while ignoring smaller recurring habits that accumulate aggressively over time.

A household may successfully avoid luxury spending while still leaking hundreds or thousands of dollars monthly through convenience-driven purchases.

Common examples include:

$18 coffee delivery orders

$40 impulse Amazon purchases

$25 same-day grocery fees

$17 streaming memberships

$120 monthly dining app spending

$300 financed electronics

unused gym subscriptions

premium convenience foods

Individually, these purchases rarely trigger concern. Most people mentally categorize them as “manageable” because each transaction appears relatively small compared to rent, mortgages, or car payments.

But modern banking apps unintentionally hide the emotional weight of spending. Swiping cards, tapping phones, and automated payments remove the visual discomfort that cash once created.

A surprising number of families spend over $1,200 monthly on non-essential convenience without realizing how large the total became.

Even households attempting to budget often underestimate how aggressively small purchases scale over a full year. A family spending an extra $45 daily across convenience apps, snacks, subscriptions, and impulse purchases can quietly lose more than $16,000 annually.

That number alone exceeds what many Americans contribute toward emergency savings.

Lifestyle Inflation Became More Aggressive Than Salary Growth

One of the biggest financial traps affecting middle income households today involves lifestyle inflation disguised as “normal adult progress.”

People naturally expect their quality of life to improve as income rises. That is reasonable. The problem begins when every raise immediately transforms into higher recurring expenses.

A promotion that increases monthly income by $600 often triggers:

a more expensive apartment,

a newer vehicle,

upgraded devices,

additional subscriptions,

higher dining spending,

premium services,

and larger financed purchases.

Within months, the extra income disappears.

Many consumers no longer experience raises as financial relief because their lifestyles expand at the exact same speed as their earnings.

Social media intensified this pressure dramatically. Daily exposure to luxury apartments, expensive vacations, designer kitchens, premium home offices, and curated lifestyles changed what many people now consider “average.”

As a result, middle class households increasingly normalize expenses that previous generations viewed as upper-middle-class luxuries.

A few years ago, financing a $1,400 smartphone might have seemed excessive. Today, monthly financing plans make those purchases feel emotionally smaller, even though the long-term cost remains significant.

The psychological effect of monthly payments often weakens spending resistance far more than people realize.

The Emotional Cost Behind Constant Financial Pressure

Money stress rarely appears only through numbers. In many households, it slowly changes emotional behavior, decision-making, and long-term planning.

Couples argue more frequently about spending.

People postpone medical appointments.

Vacation guilt increases.

Unexpected expenses feel emotionally exhausting instead of manageable.

Many workers now remain trapped in jobs they dislike mainly because their monthly obligations became too heavy to comfortably survive income interruptions.

This creates a dangerous cycle.

High stress encourages convenience spending because people feel mentally drained. Then the additional spending creates even more financial pressure later.

Someone working long hours may justify:

more delivery apps,

more impulse shopping,

more convenience services,

and more financed purchases

simply because exhaustion reduces financial discipline.

Financial fatigue became one of the most underestimated consequences of modern consumer culture.

The issue becomes especially noticeable among younger adults balancing:

student loans

high rent

insurance costs

car payments

rising grocery bills

digital subscriptions

childcare expenses

Many people are not financially reckless. They are simply navigating an economy where convenience is constantly marketed as emotional relief.

Buying Cheap Often Creates More Expensive Problems Later

An interesting contradiction appeared in modern consumer behavior. While many households aggressively search for discounts, they sometimes create larger financial losses by prioritizing short-term savings over long-term durability.

Cheap furniture may require replacement within two years.

Low-cost electronics often fail earlier.

Fast fashion purchases accumulate rapidly despite poor quality.

Budget appliances can generate repeated repair costs.

Trying to save money immediately sometimes produces far higher costs over time.

This became particularly visible in housing and automotive expenses.

A buyer choosing an unreliable used vehicle mainly because the monthly payment appears lower may later face:

repair bills

higher insurance

missed work

towing costs

credit card debt

stress-related financial decisions

Meanwhile, another buyer spending slightly more upfront on reliability may ultimately spend far less across five years.

The same principle affects home purchases, furniture, technology, appliances, and even grocery spending.

Consumers increasingly face a difficult balancing act between affordability today and durability tomorrow.

The Subscription Economy Quietly Changed Household Budgets

Ten years ago, most recurring bills involved housing, utilities, insurance, and phone service.

Today, many households manage dozens of smaller recurring charges simultaneously.

Examples now include:

streaming services

cloud storage

fitness apps

meal subscriptions

AI tools

music platforms

gaming memberships

delivery subscriptions

software access

smart home services

Many consumers lose track of these expenses because automatic billing removes spending visibility.

A person paying:

$14.99

$8.99

$19.99

$11.99

$24.99

across multiple services may emotionally interpret those purchases as “small,” even while spending over $250 monthly.

Recurring digital spending became one of the easiest ways for middle income households to slowly lose financial flexibility without noticing immediately.

That flexibility matters far more than many people realize.

Emergency savings, investment contributions, debt reduction, and retirement planning all become harder when recurring expenses quietly consume future income before it even arrives.

Financial Stability Now Depends More on Awareness Than Income Alone

One of the biggest misconceptions about personal finance is the belief that income automatically solves money problems.

Higher income absolutely helps. But spending behavior, recurring obligations, and financial awareness often matter just as much.

Some households earning $70,000 annually maintain stronger financial stability than households earning $140,000 because they control recurring expenses more carefully.

Others avoid lifestyle inflation entirely after raises, choosing instead to:

increase savings,

eliminate debt,

build emergency funds,

invest consistently,

or reduce financial stress.

Long-term financial stability usually comes from controlled habits rather than dramatic financial moves.

That does not mean people should avoid enjoying life or eliminate all convenience spending. Modern services genuinely save time and reduce stress in certain situations.

The difference comes from intentional spending versus automatic consumption.

Consumers who actively understand where their money goes each month usually maintain far more financial flexibility than those reacting emotionally to convenience-driven spending patterns.

FAQ

Why do middle class families still feel financially stressed despite decent income

Rising living costs, recurring subscriptions, financed purchases, inflation, and lifestyle inflation often expand faster than salary growth. Many households experience strong income on paper while still carrying heavy monthly obligations.

What is lifestyle inflation

Lifestyle inflation happens when spending increases alongside income. Instead of using raises to improve savings or reduce debt, people gradually upgrade housing, vehicles, subscriptions, and daily habits until additional income disappears.

Are small purchases really that damaging financially

Individually, usually not. The problem comes from frequency and accumulation. Daily convenience spending can quietly total thousands of dollars annually without triggering immediate concern.

What financial habit helps most with long-term stability

Tracking recurring expenses consistently is one of the most effective habits. People often focus heavily on large purchases while underestimating how much monthly convenience spending affects savings and debt levels.

Conclusion

Modern financial pressure rarely arrives through one catastrophic decision. More often, it builds quietly through dozens of normalized habits that slowly reduce flexibility month after month.

Convenience itself is not the enemy. Many services genuinely improve quality of life and save valuable time. The problem begins when automatic spending replaces intentional decision-making.

Middle class financial stress increasingly comes from invisible accumulation rather than obvious irresponsibility.

And for many households, recognizing that pattern becomes the first meaningful step toward regaining financial breathing room again.